When most people think of banking, they think of commercial banks — institutions that take deposits and make loans. But a huge portion of modern finance happens outside traditional banks in what’s known as the shadow banking system.

Despite the name, it’s not necessarily illegal. It’s simply less regulated, less visible, and often more complex.

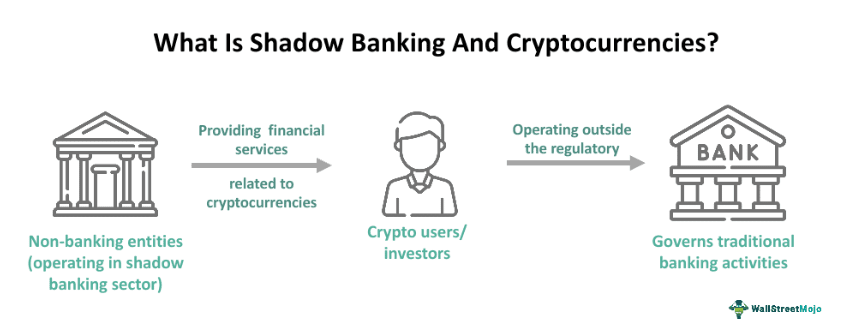

What Is Shadow Banking?

Shadow banking refers to financial institutions and activities that perform bank-like functions without being regulated as banks.

These include:

-

Hedge funds

-

Money market funds

-

Private equity firms

-

Repo market participants

-

Structured investment vehicles

-

Mortgage companies and fintech lenders

They provide credit, liquidity, and maturity transformation — but without the same capital and safety requirements as traditional banks.

Why It Exists

Shadow banking grew because traditional banking regulations became stricter after financial crises. As banks faced higher capital requirements, credit activity migrated elsewhere.

This created a parallel system that can:

-

Move faster

-

Use more leverage

-

Avoid some regulatory costs

-

Take on higher risks

In good times, shadow banking boosts credit and liquidity. In bad times, it can amplify instability.

The 2008 Lesson

The global financial crisis revealed how dangerous shadow banking can be. Mortgage-backed securities, structured investment vehicles, and off-balance-sheet funding played a central role.

When confidence collapsed, funding vanished overnight. Institutions that weren’t technically banks still needed bailouts — proving they were systemically important.

Why Regulators Struggle to See It

Shadow banking is harder to monitor because:

-

Activities are fragmented across markets

-

Transactions are often short-term and complex

-

Entities operate across borders

-

New structures constantly emerge

This makes systemic risk harder to detect in advance.

Why It Still Matters Today

Shadow banking is now larger than traditional banking in many economies. It plays a major role in:

-

Corporate credit

-

Real estate financing

-

Emerging market capital flows

-

Hedge fund leverage

While it increases financial efficiency, it also creates blind spots. The next financial crisis may not start at a traditional bank — it may start in the shadows.