The Invisible Pipes: Why the Repo Market is the Heart of Global Finance

In the towering glass skyscrapers of Wall Street, the most critical transactions don’t involve complex stock options or high-profile IPOs. Instead, they involve “repos”—a term few outsiders understand, but one that keeps the global economy from seizing up. If the financial system is a house, the stock market is the paint and the banking system is the frame, but the repurchase agreement (repo) market is the plumbing. It isn’t glamorous, and you only notice it when it breaks—but when it does, the mess is catastrophic.

What Exactly is a Repo?

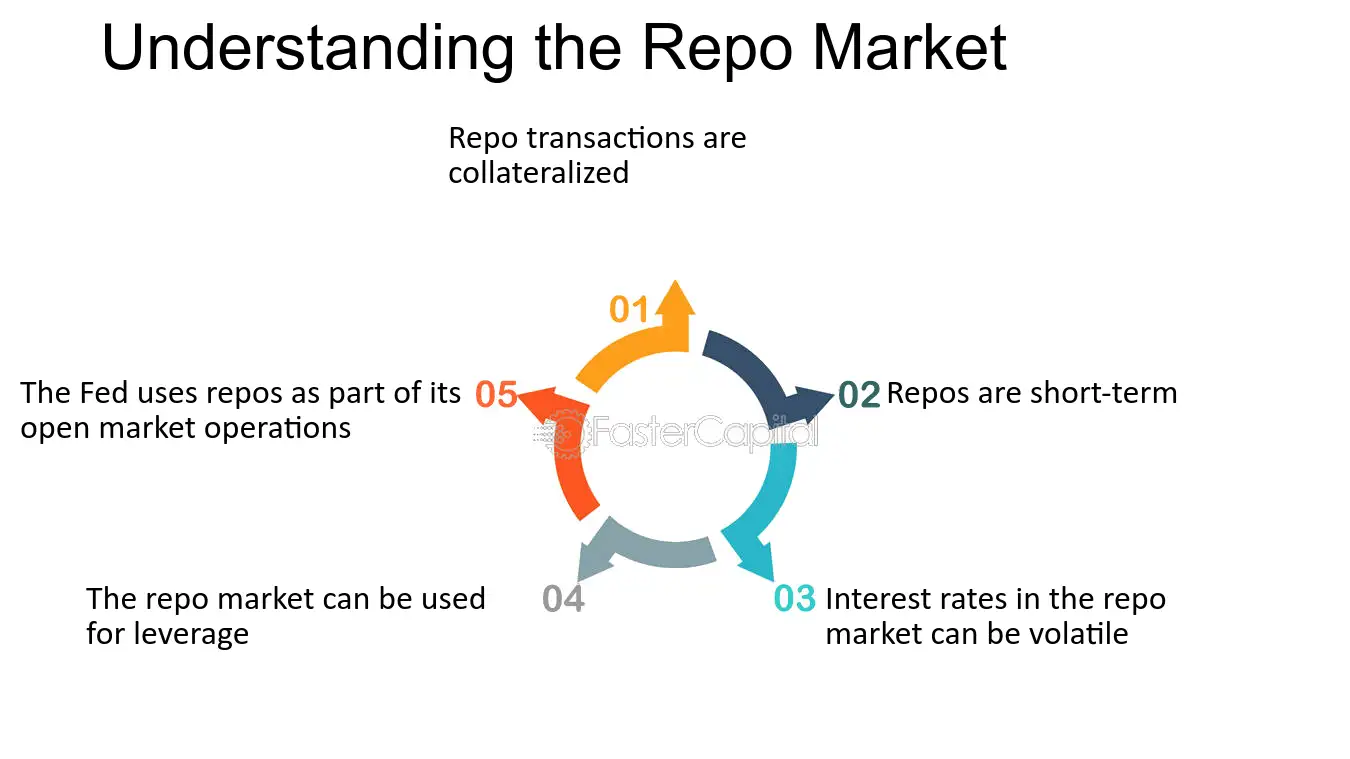

A repurchase agreement is essentially a sophisticated, short-term collateralized loan. In a typical repo transaction, one party (such as a bank or hedge fund) sells a high-quality security—usually a U.S. Treasury bond—to another party (like a money market fund) for cash. Simultaneously, the seller agrees to buy that security back the very next day at a slightly higher price.

The difference between the sale price and the repurchase price represents the interest rate, known as the repo rate. For the borrower, it’s a way to get quick cash; for the lender, it’s a safe way to earn a tiny bit of interest on idle funds, secured by the safest collateral in the world.

Why the System Depends on “Plumbing”

The repo market handles trillions of dollars in transactions every single day. Its primary job is to provide liquidity. Banks use it to manage their daily cash flow needs, ensuring they have enough reserves to meet regulatory requirements. Hedge funds use it to gain leverage, borrowing against their holdings to increase their buying power. Most importantly, the Federal Reserve uses the repo market as a tool to control short-term interest rates.

When the “plumbing” is clear, money flows effortlessly through the economy. But because these loans are often “overnight,” the entire system relies on absolute confidence.

The 2019 Warning Shot

The fragility of this system was laid bare in September 2019. Unexpectedly, the repo rate spiked from around 2% to nearly 10% in a single day. The “plumbing” had clogged; lenders suddenly stopped providing cash, and the demand for overnight loans far outstripped the supply. The financial system began to seize up, forcing the Federal Reserve to intervene by injecting billions of dollars into the market to keep rates from spiraling. It was a stark reminder that even the “safest” markets can become fragile under pressure.

A Hidden Systemic Risk

The repo market represents a unique systemic risk because of its short-term nature. Unlike a ten-year loan, a repo must be “rolled over” every 24 hours. If lenders become nervous about the economy or the value of the collateral, they can simply stop lending instantly. This “run on the repo” was a major factor in the 2008 financial crisis, leading to the collapse of firms like Bear Stearns.

Today, central banks have become the ultimate “plumbers,” acting as a permanent backstop to ensure that the repo market never stays clogged for long. As long as the repo market functions, the world keeps turning—but its complexity remains a silent, shifting foundation beneath the global economy.