For most people, the idea of banking is simple and intuitive. Savers deposit money. Banks safeguard it. Borrowers take loans from this pool of savings. It feels logical—almost commonsense. Yet this mental model is largely wrong. In modern economies, banks do not merely move money around. They create it.

This fact is rarely emphasized outside economics textbooks, but it sits at the heart of how modern capitalism functions. Understanding how banks create money helps explain everything from economic booms and busts to inflation, financial crises, and why bank runs are so dangerous.

The Myth of “Lending Out Deposits”

The popular image of banking belongs to an earlier era. In that world, a bank acted like a warehouse. You deposited $1,000. The bank kept it safe. Someone else borrowed a portion of it. The total amount of money in the system stayed the same.

That description no longer fits reality.

Today’s banks operate under a system known as fractional reserve banking. Under this framework, banks are only required to keep a fraction of their customers’ deposits as reserves—either as physical cash or as balances held at the central bank. The rest can be used to support lending and other financial activities.

But the key insight goes even further: banks do not wait for deposits in order to lend. Instead, lending itself creates deposits.

A Loan That Creates Money

Consider what happens when you take out a $20,000 car loan.

The bank does not go to a vault, count out twenty thousand-dollar bills, and hand them to you. In fact, no physical cash may move at all. Instead, the bank approves the loan and credits your account with $20,000 in digital balances.

At that moment, something remarkable happens. The total amount of money in the economy increases by $20,000.

From your perspective, you now have new money to spend. From the bank’s perspective, it has created an asset (your loan, which you must repay with interest) and a liability (the deposit in your account). Both appear on the bank’s balance sheet simultaneously.

This is why economists say that commercial banks create money “out of thin air”—though a more precise description would be “out of balance sheets.”

What About Reserves?

If banks can create money by issuing loans, what stops them from lending infinitely?

The answer lies in constraints—but not quite the ones people usually imagine.

Banks are subject to reserve requirements, capital requirements, liquidity rules, and regulatory supervision. They must hold sufficient high-quality assets and central bank reserves to meet withdrawals and payments. They must also ensure borrowers are creditworthy, because bad loans destroy bank capital.

Importantly, in many modern economies, reserve requirements are no longer the binding constraint they once were. Central banks supply reserves as needed to keep the payment system functioning smoothly. In practice, banks are constrained more by profitability, risk management, and regulation than by the raw availability of reserves.

In other words, banks do not lend because they have reserves; they acquire reserves because they have lent.

Money as a Web of Promises

This system leads to a profound but unsettling conclusion: most money today is not physical cash. It is a network of promises.

Your bank deposit is not money in the traditional sense. It is a claim on your bank. The bank promises to convert that digital balance into cash or transfer it elsewhere on demand. The bank, in turn, relies on the central bank as the ultimate backstop—able to provide liquidity in times of stress.

Physical cash exists, but it represents only a small fraction of the total money supply. Measures such as M2—which include bank deposits and other near-money instruments—are dominated by these digital entries created through lending.

Money, in the modern system, is best understood not as a thing but as a relationship.

Why Bank Runs Are So Dangerous

This architecture explains why bank runs are uniquely destructive.

Because deposits are created through lending, banks do not—and cannot—hold enough cash to repay every depositor at once. If all customers demanded physical money simultaneously, even a perfectly solvent bank would fail.

Bank runs are not just about fear; they are about arithmetic.

Historically, this fragility led to recurring financial panics. Modern systems attempt to manage this risk through deposit insurance, central bank lender-of-last-resort facilities, and strict supervision. These mechanisms are designed to preserve confidence—because confidence is the glue holding the system together.

Once confidence breaks, the abstract promises that define modern money can unravel with terrifying speed.

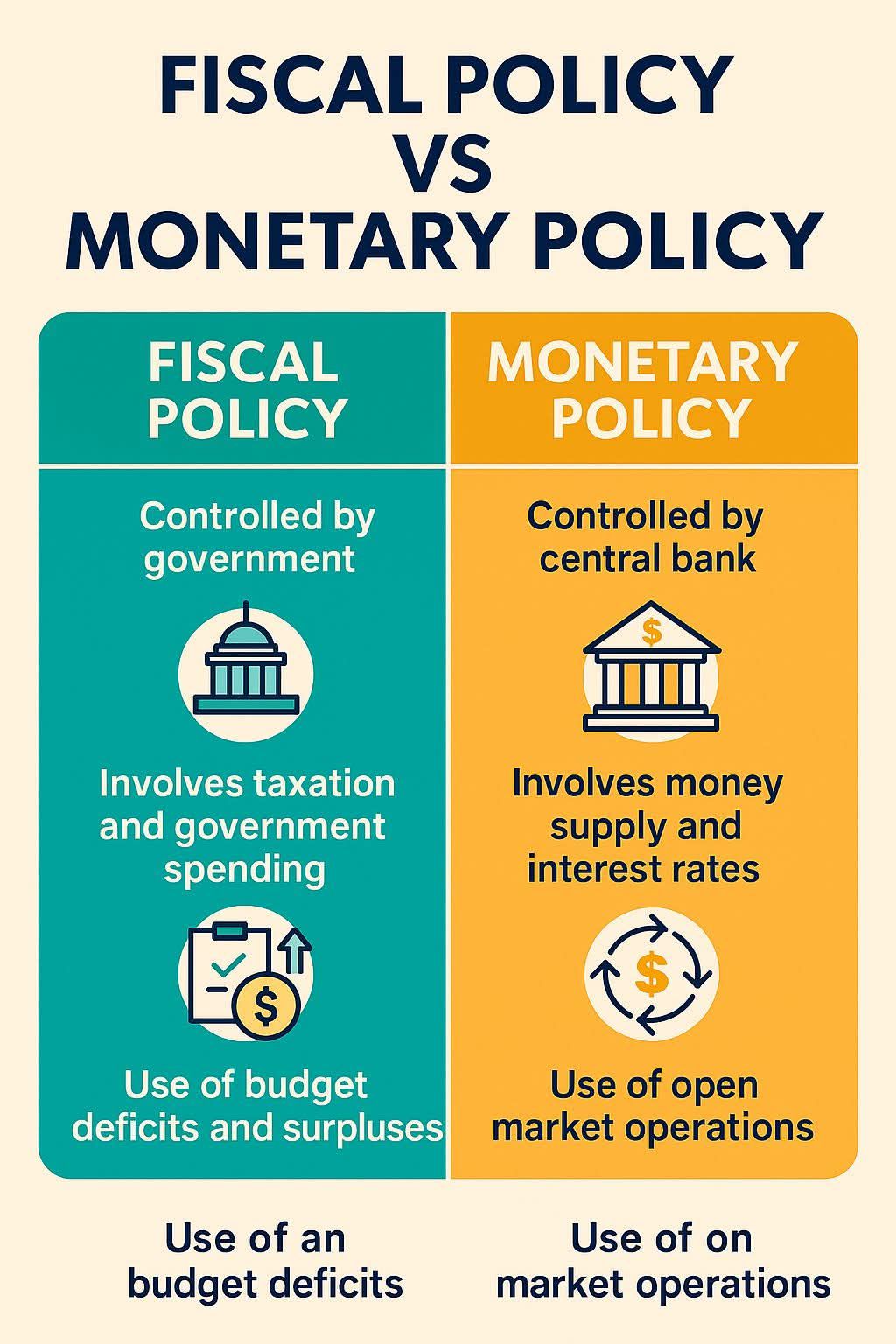

The Central Bank’s Role

Central banks sit at the apex of this system.

Contrary to popular belief, central banks do not directly control the money supply in a mechanical way. They do not “print money” every time the economy needs more. Instead, they influence the price of money—interest rates—and provide liquidity to ensure stability.

When central banks lower interest rates, borrowing becomes cheaper. Banks issue more loans. More deposits are created. The money supply expands. When rates rise, lending slows, and money creation decelerates.

In this sense, commercial banks are the primary engines of money creation, while central banks act as traffic controllers—trying to manage speed, prevent crashes, and stabilize the system.

Power and Consequences

The ability of banks to create money gives them immense power over the real economy. Credit creation fuels business investment, housing markets, consumer spending, and asset prices. When credit flows freely, economies expand. When it contracts, recessions often follow.

This is why financial crises are so damaging. They are not just failures of markets; they are breakdowns in the money-creation process itself.

It is also why debates about banking regulation, interest rates, and financial stability are ultimately debates about who gets access to newly created money—and on what terms.

A Digital Printing Press

If one were to visualize this system, a fitting image might be a digital printing press inside a commercial bank. Instead of ink and paper, it runs on legal contracts and accounting entries. A loan agreement goes in. Digital dollar signs come out.

The metaphor is imperfect but revealing. Money is not printed by governments alone, nor hoarded in vaults waiting to be redistributed. It is continuously created and destroyed through lending, repayment, and default.

Understanding this does not make the system less strange—but it does make it more honest.

The Takeaway

Modern money is not what most people think it is. Banks do not merely lend savings; they create purchasing power. Deposits are promises. Cash is the exception, not the rule.

This system has powered extraordinary economic growth, but it also carries inherent fragility. It depends on trust—trust in banks, trust in central banks, and trust in the legal and political systems that stand behind them.

Once you see money this way, financial headlines look different. Inflation, crises, and policy decisions are no longer abstract events. They are shifts in a vast, invisible web of promises that quietly shapes everyday life.