In the complex world of the U.S. tax code, few terms spark as much partisan fire as “carried interest.” Often labeled a “loophole” by critics and a “vital incentive” by proponents, carried interest sits at the intersection of high finance and public policy. It is more than just an accounting quirk; it is a symbol of a fundamental tension in modern economics: should we tax the money people work for the same way we tax the money people invest?

What exactly is Carried Interest?

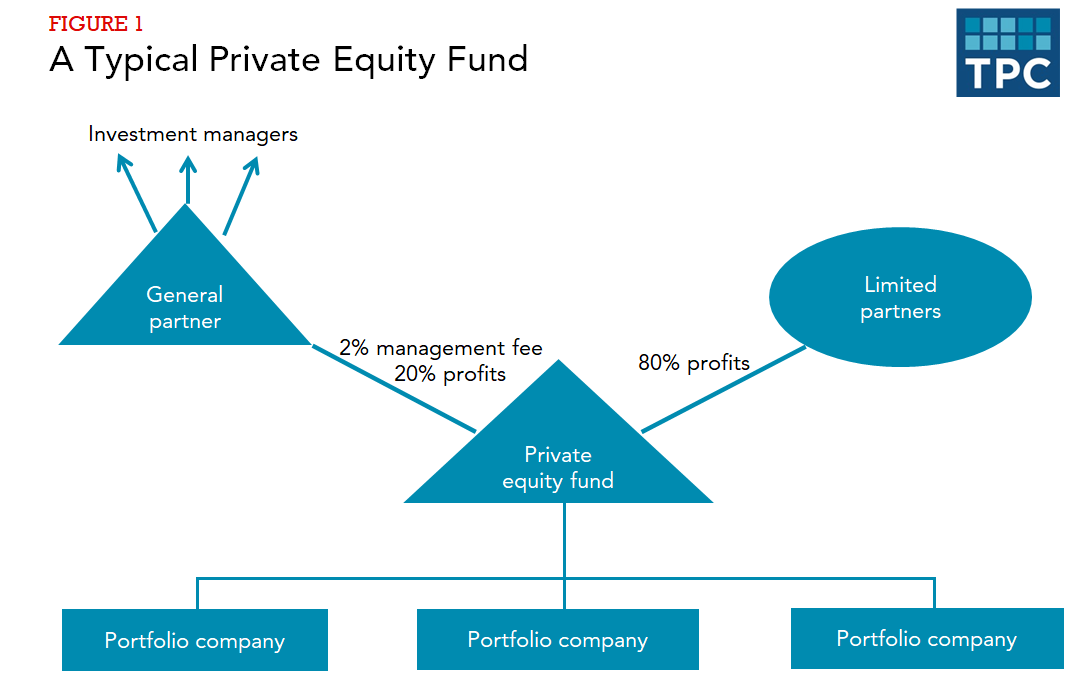

To understand the controversy, one must first understand the “2 and 20” fee structure common in private equity, venture capital, and hedge funds. Managers typically charge a 2% management fee (taxed as regular income) and take a 20% share of the fund’s total profits. This 20% share is the carried interest.

The controversy arises not from the payment itself, but from how it is categorized by the IRS. Currently, if the fund holds its investments for a certain period (usually three years), that 20% profit share is taxed as long-term capital gains rather than ordinary income.

The Tax Gap

The mathematical impact of this classification is profound. While the top bracket for ordinary income is 37%, the top long-term capital gains rate is only 20% (plus a 3.8% net investment income tax). This allows some of the wealthiest individuals on Wall Street to pay a lower effective tax rate than many “high-earning” professionals, such as surgeons or specialized engineers, whose income is derived strictly from a salary.

The Battle of Perspectives

The defense of carried interest rests on the idea of “skin in the game.” Proponents argue that fund managers are not just employees; they are entrepreneurs who take significant risks. By taxing their rewards at a lower rate, the government encourages the long-term investment and risk-taking necessary to fuel innovation and restructure struggling companies. From this perspective, carried interest is a return on investment, not a fee for service.

Critics, however, view this as a semantic sleight of hand. They argue that because fund managers are often investing other people’s money rather than their own, the 20% profit share is essentially a performance-based bonus. In any other industry—from a salesperson’s commission to a CEO’s stock-option package—performance pay is taxed as ordinary income. Critics contend that the current system unfairly prioritizes capital over labor, deepening wealth inequality and distorting the tax base.

Why the “Loophole” Persists

Despite being a frequent target for reform on both sides of the political aisle, carried interest has proven remarkably resilient. Its survival is largely attributed to the aggressive lobbying efforts of the financial sector and a genuine fear among lawmakers that changing the rules could disincentivize investment in the American economy.

As we look toward future tax reforms, carried interest remains the ultimate litmus test for how a society values different types of wealth. Is it a necessary engine for economic growth, or a relic of a system tilted in favor of the ultra-wealthy? Until the tax code treats a dollar earned through labor the same as a dollar earned through investment, the debate will continue to rage.