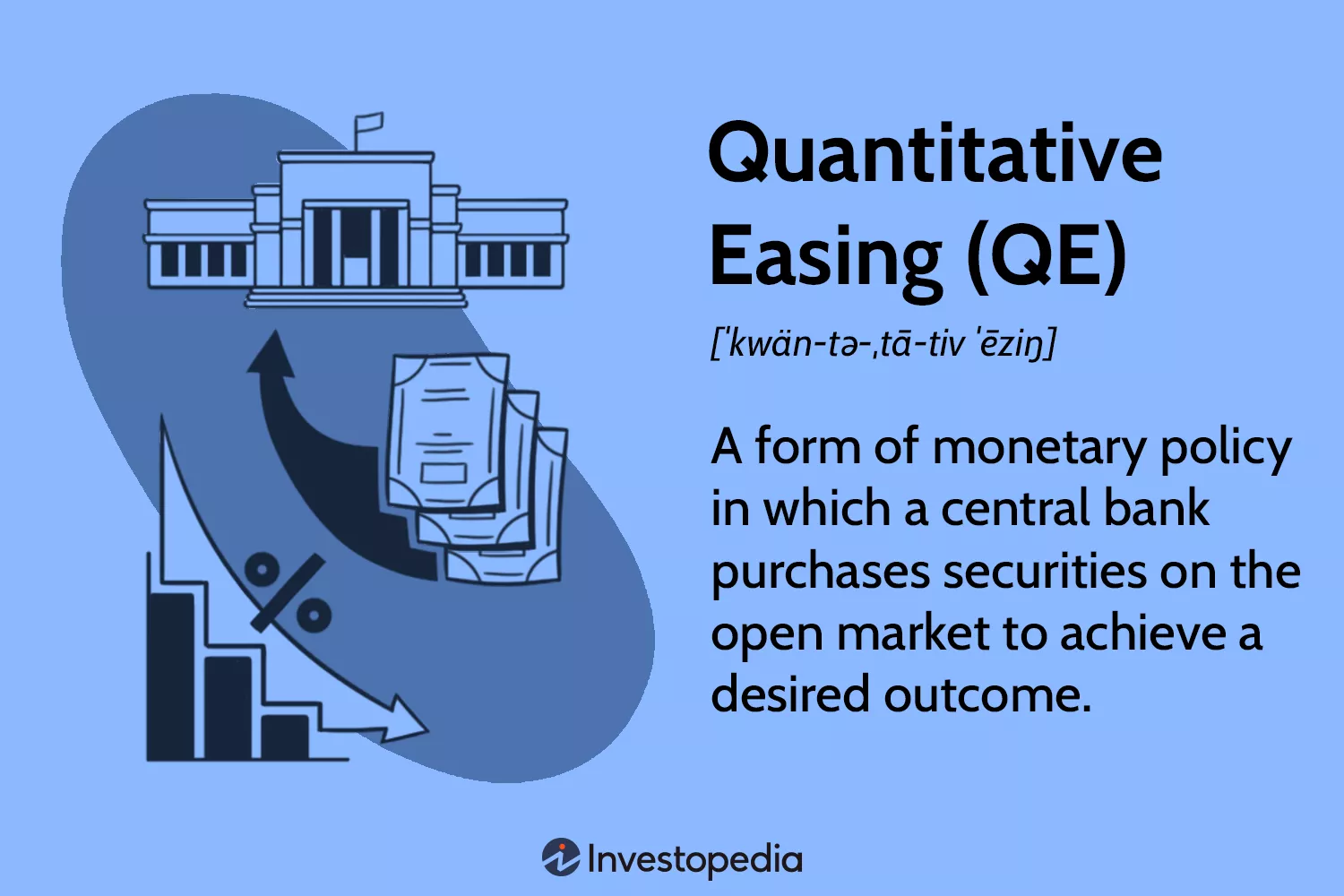

For decades, the primary lever of monetary policy was the adjustment of interest rates. When the economy slowed, central banks lowered rates to encourage borrowing; when it overheated, they raised them. However, the 2008 financial crisis and the subsequent COVID-19 pandemic revealed a limitation to this traditional approach: the “zero lower bound.” When interest rates hit zero, central banks can no longer cut them to stimulate growth. To bypass this dead end, policymakers turned to Quantitative Easing (QE)—a process often described as “printing money,” though it involves neither a printing press nor physical currency.

At its core, QE is an unconventional monetary policy where a central bank creates digital money to purchase government bonds or other financial assets from the open market. The process begins with the central bank electronically increasing its own balance sheet. With this “new” money, it buys bonds from commercial banks and private institutions. This influx of demand drives bond prices up and, conversely, pushes bond yields (interest rates) down. By flooding the financial system with liquidity, the central bank aims to lower the cost of borrowing across the entire economy, encouraging businesses to expand and consumers to spend.

The mechanics of QE primarily target the financial sector rather than the general public. When a central bank buys assets from commercial banks, it increases those banks’ “excess reserves.” The theory is that banks, now sitting on a mountain of digital cash that earns little interest, will be incentivized to lend that money to people and businesses. However, QE does not directly put a paycheck into a consumer’s pocket; it filters through the pipes of the financial system, hoping to create a “trickle-down” effect of credit availability.

While QE can prevent a total economic collapse and ward off deflation, it carries significant side effects. Because QE drives up the price of financial assets—stocks, bonds, and real estate—it tends to benefit those who already own such assets. This has led to a widening of wealth inequality, as the “wealth effect” inflates the portfolios of the affluent while the cost of living and housing continues to rise for everyone else. Furthermore, by artificially suppressing interest rates, QE can distort market signals, leading to “asset bubbles” where prices no longer reflect the fundamental value of a company or property.

Perhaps the most daunting aspect of QE is its transition from “emergency medicine” to a permanent fixture of the financial diet. What was once a radical, temporary measure has become an expected response to any market volatility. This creates a “moral hazard,” where investors take excessive risks under the assumption that the central bank will always step in to provide a liquidity backstop.

As we look toward the future, the challenge for central banks is no longer just how to start the QE engine, but how to turn it off without crashing the global economy. The transition from “Easy Money” to a normalized environment remains the great experiment of the 21st century.