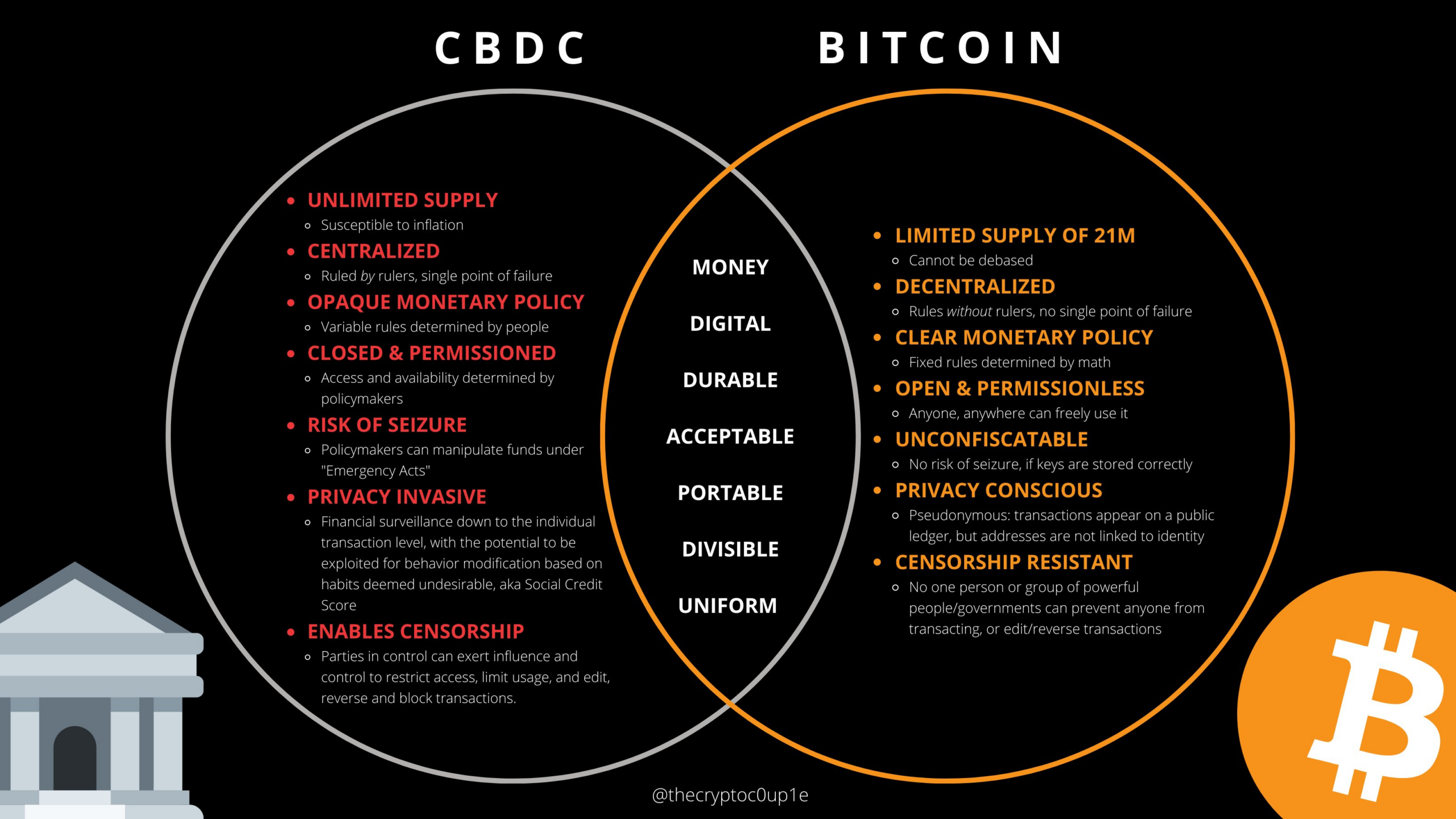

The advent of Bitcoin in 2009 was predicated on a radical promise: the separation of money and state. By utilizing decentralized ledger technology, cryptocurrency offered a vision of financial freedom where transactions were peer-to-peer and immune to government intervention. However, a decade later, the global financial landscape is witnessing a counter-revolution. Instead of yielding to decentralization, nation-states are co-opting the technology to create Central Bank Digital Currencies (CBDCs). While Bitcoin sought to take money out of government hands, CBDCs represent the ultimate consolidation of state power over the digital economy.

At its core, a CBDC is a digital form of a country’s fiat currency, issued and regulated directly by the central bank. Unlike Bitcoin, which relies on a distributed network of “miners” and an algorithmic supply cap, a CBDC is a centralized liability of the government. It is legally equivalent to physical cash but exists entirely in a digital ledger. Currently, over 100 countries—representing over 90 percent of global GDP—are in various stages of researching, piloting, or deploying these digital assets.

The motivations behind the government-led push for CBDCs are multifaceted. On a practical level, they promise to modernize aging financial infrastructures by making domestic and cross-border payments faster and cheaper. They also offer a pathway toward greater financial inclusion, providing unbanked populations with access to a digital payment system without requiring a traditional commercial bank account. Furthermore, as physical cash usage declines, central banks view CBDCs as a way to maintain the “public anchor” of money, ensuring that private payment providers do not hold a monopoly over the movement of value.

However, the shift from crypto-decentralization to CBDC-centralization introduces profound geopolitical and social consequences. From a geopolitical perspective, the “digital yuan” in China is a prime example of how digital currency can be leveraged to challenge the global dominance of the U.S. dollar. By creating an efficient, state-backed digital payment network, nations can bypass Western-led financial systems like SWIFT, thereby insulating themselves from international sanctions and strengthening their monetary sovereignty.

The most significant concern regarding CBDCs, however, lies in the “big tradeoff” between efficiency and liberty. Cryptocurrency is characterized by pseudonymity and censorship resistance; CBDCs, by contrast, are designed for transparency and traceability. Because the central bank sits at the heart of every transaction, a CBDC provides the state with an unprecedented level of surveillance into the private lives of its citizens. In a fully realized CBDC ecosystem, money becomes “programmable.” Governments could, in theory, implement negative interest rates, set expiration dates on funds to force spending, or freeze the assets of political dissidents with the click of a button.

Ultimately, CBDCs represent a fork in the road for the future of money. While they offer the allure of a more streamlined, inclusive, and modern financial system, they do so at the potential cost of absolute financial privacy. As the world moves toward a digital-first economy, the struggle is no longer just between paper and pixels, but between two competing ideologies: a decentralized future where money is a tool for individual autonomy, or a centralized one where it is an instrument of state control.