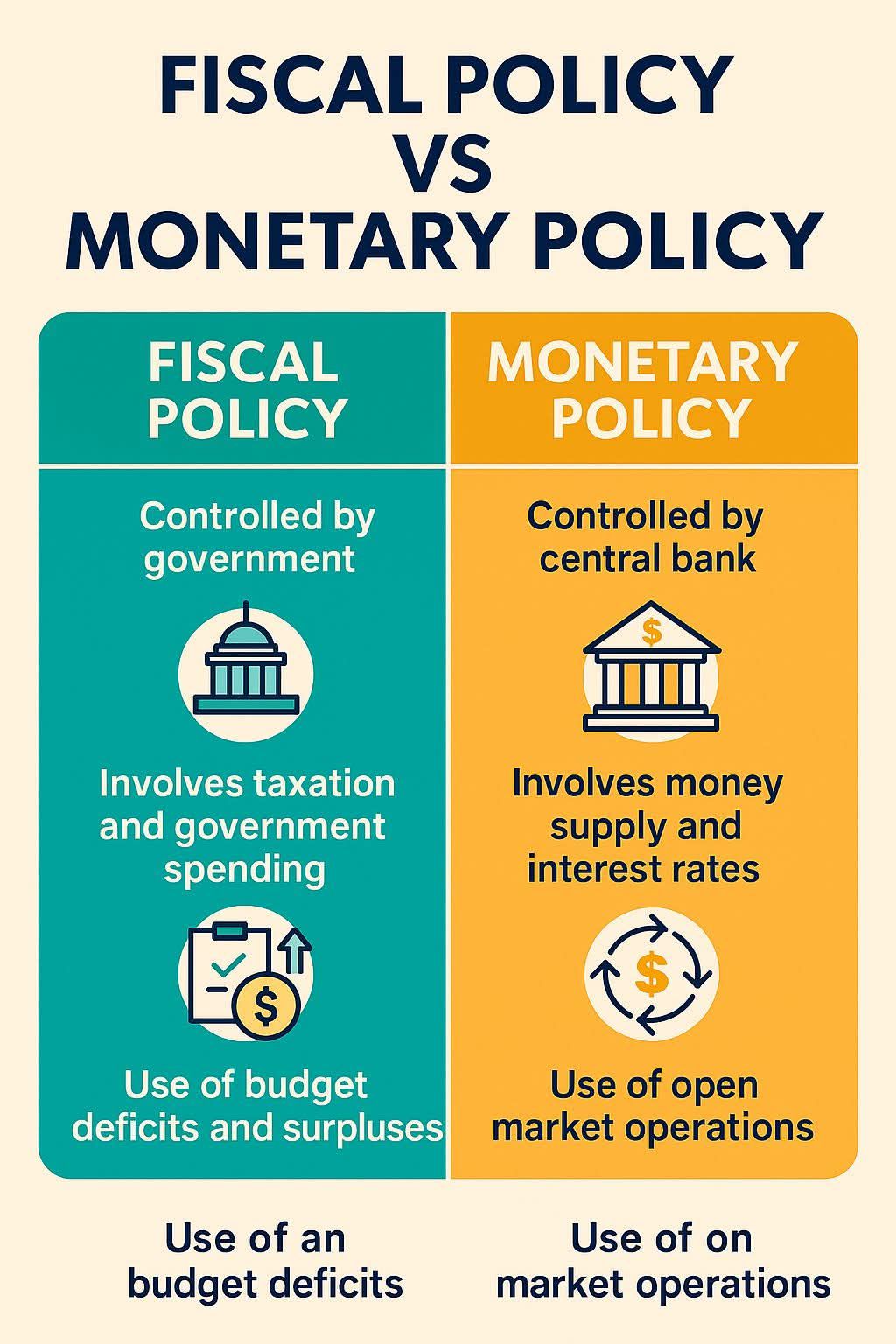

Fiscal vs Monetary Policy: Who Really Drives the Economy?

When economies slow down or inflation spikes, the debate almost always turns to policy. Should governments spend more? Should central banks raise or cut interest rates? At the heart of this discussion lies the distinction between fiscal policy and monetary policy—two powerful tools that shape economic outcomes in very different ways.

While both aim to stabilize growth, employment, and prices, their mechanisms, timelines, and political constraints vary sharply.

What Is Fiscal Policy?

Fiscal policy refers to government decisions on spending, taxation, and borrowing. When governments increase spending or cut taxes, they inject demand into the economy. When they raise taxes or reduce spending, they withdraw demand.

Fiscal policy is typically used to:

- Stimulate growth during recessions

- Redistribute income

- Fund long-term investments such as infrastructure, education, and defense

The strength of fiscal policy lies in its directness. A government building roads or sending cash transfers immediately affects incomes and employment. This was evident during the 2008 financial crisis and the 2020 pandemic, when large fiscal packages prevented deeper collapses in demand.

However, fiscal policy has weaknesses. It is politically constrained, slow to implement, and often influenced by electoral incentives rather than economic timing. Poorly designed fiscal expansions can also increase public debt without improving productivity.

What Is Monetary Policy?

Monetary policy is controlled by central banks, which manage interest rates, liquidity, and credit conditions. The most common tools include:

- Setting policy interest rates

- Open market operations

- Quantitative easing or tightening

Monetary policy primarily influences the economy indirectly, by shaping borrowing costs, asset prices, and expectations. Lower interest rates encourage spending and investment; higher rates cool inflation and asset bubbles.

Its main advantage is speed and flexibility. Central banks can act quickly and independently, without waiting for legislative approval. This responsiveness has made monetary policy the first line of defense against short-term economic shocks.

But monetary policy also has limits. It works poorly when interest rates are already near zero, and it tends to benefit asset owners more than wage earners—raising concerns about inequality.

Which Is More Effective?

The effectiveness of fiscal versus monetary policy depends heavily on context.

- In deep recessions, fiscal policy tends to be more powerful because monetary transmission channels weaken.

- In inflationary environments, monetary tightening is often more effective and politically feasible.

- In normal cycles, monetary policy dominates day-to-day stabilization.

Post-2008 and post-2020 experiences show that policy coordination matters most. Monetary policy can stabilize markets, but fiscal policy is often needed to support real incomes and employment.

Bottom Line

Fiscal and monetary policy are not rivals—they are complements. Monetary policy excels at speed and signaling, while fiscal policy delivers scale and targeting. Economies perform best when both are aligned, credible, and responsive to underlying conditions rather than political pressure.