1. The Great Transition: From Growth to Stability

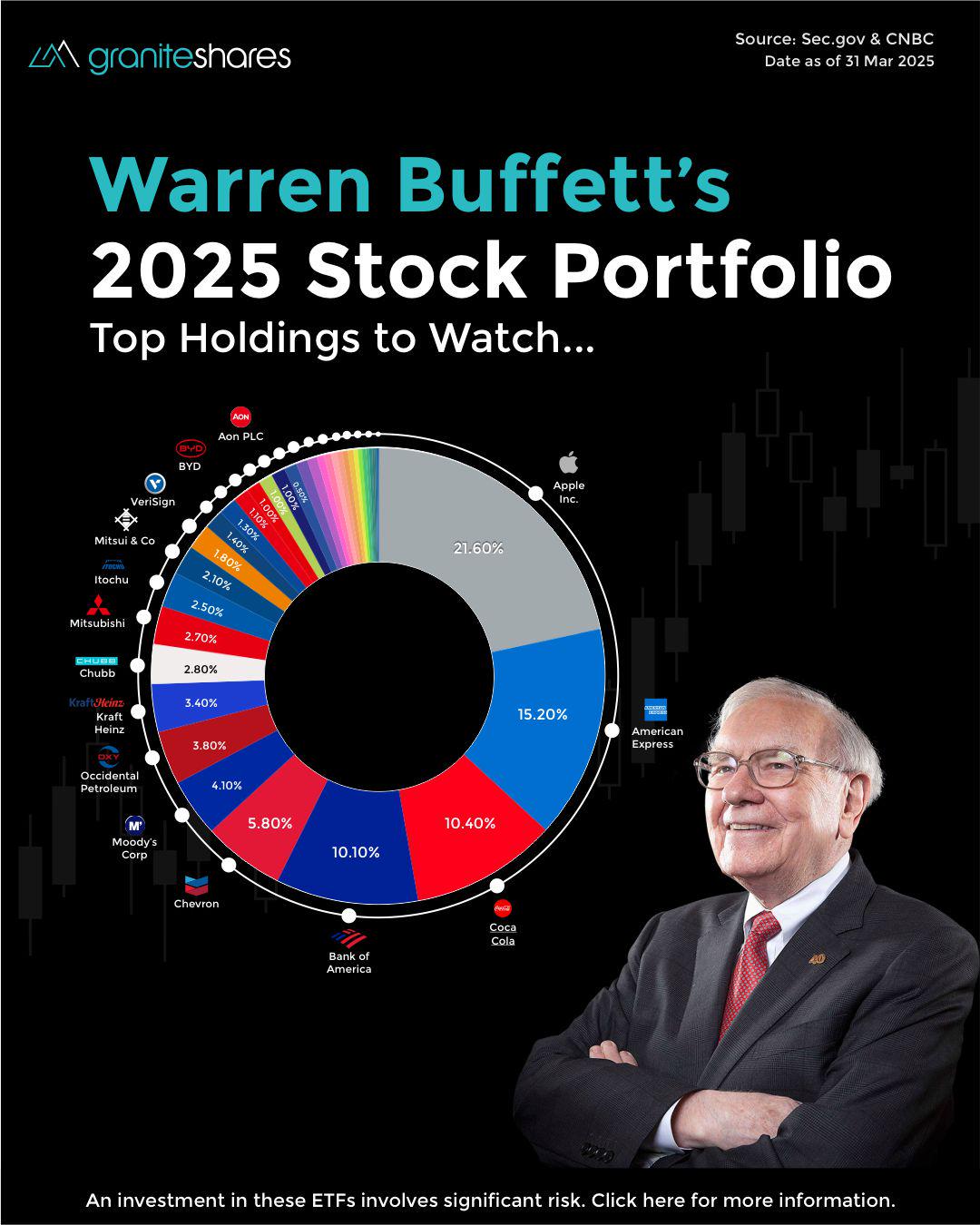

The most striking feature of the Berkshire portfolio in 2026 is its sheer concentration. While the “Neighbor” might diversify into fifty different small bets, Berkshire remains a high-conviction machine. As of the latest filings, roughly 74% of the $317 billion portfolio is tied up in just eight “Unstoppable” companies.

However, the “Forward-Looking” nature of this portfolio has shifted. For nearly a decade, Apple was the beating heart of Berkshire’s growth. But between 2024 and late 2025, a massive pruning occurred. Berkshire reduced its Apple stake by over 70%, selling hundreds of millions of shares. This wasn’t a vote of “no confidence” in the iPhone; it was a surgical rebalancing. Apple remains a top holding (roughly 20-22%), but it is no longer the single pillar holding up the roof. The message is clear: even a “wonderful business” can become too heavy for the scale.

2. The Financial Fortress: The American Express Ascent

As Apple’s weight was trimmed, a familiar face rose to take its place in the spotlight: American Express (AXP). Currently making up nearly 18-20% of the portfolio, Amex has become the quintessential “Buffett-Abel” stock.

Why Amex? In our current macro-climate of “Policy Capture” and fluctuating interest rates, American Express holds a unique “Moat.” It is both a payment processor and a lender, catering to a premium demographic that is more resilient to inflation. In the language of the cardiac surgeon, Amex is the “Stable Rhythm” of the portfolio. It generates massive cash flow and, perhaps more importantly, its brand power allows it to raise fees without losing customers. It is a “dividend machine” that Berkshire has held since 1991, and by mid-2026, it may very well be the largest single holding by market value.

3. Energy and the “Visible Thumb” of Policy

One cannot analyze Berkshire in 2026 without looking at the Energy Sector. The portfolio has become increasingly heavy in “Old World” energy, specifically Chevron (CVX) and Occidental Petroleum (OXY). Together, these make up nearly 10% of the invested assets.

This is where the “Policy-Captured” market theory becomes visible. Berkshire’s aggressive accumulation of Occidental Petroleum (reaching over 265 million shares) and its recent $9.7 billion acquisition of OxyChem (completed in early January 2026) show a bet on Domestic Energy Security.

[Image: A bar chart showing the growth of Energy as a percentage of Berkshire’s portfolio from 2022 to 2026]

Buffett and Abel aren’t just betting on oil prices; they are betting on the infrastructure of energy. Occidental is not just a driller; it’s a chemical and carbon-capture play. This is “Forward-Looking” in a very specific sense: it anticipates a future where the government heavily subsidizes carbon management and domestic production.

4. The Defensive Guard: Coca-Cola and Chubb

If the tech and energy holdings are the “Offense,” then Coca-Cola (KO) and Chubb (CB) are the “Defense.”

-

Coca-Cola: Held since 1988, it remains a pillar at ~9-10% of the portfolio. The math here is staggering: Berkshire’s cost basis is roughly $3.25 per share, yielding an annual dividend return on cost of nearly 62%. It is the ultimate “Neighborly” stock—predictable, global, and inflation-hedged.

-

Chubb Limited: A newer “Secret Stake” that was revealed in 2024. As an insurance colossus, Chubb fits Berkshire’s core competency. In a world of rising climate risks and “Policy-Captured” insurance markets, Chubb’s ability to price risk accurately makes it a “Surgeon’s Tool” for stability. It now commands over 3% of the portfolio.

5. The Banking Retreat

A notable trend in the 2025-2026 data is the continued paring of bank stocks. While Bank of America (BAC) remains a top-three holding (at ~10-11%), Berkshire has been actively selling. Over 465 million shares of BAC were offloaded in the last eighteen months.

This retreat signals a wary eye on the “Policy Capture” we discussed earlier. When the banking sector becomes a tool for government liquidity management, the “Intrinsic Value” becomes harder to calculate. Berkshire is staying in the room, but they are standing closer to the exit.

6. The “Small Bets” and the New Guard

Beneath the giants, we see the fingerprints of the “New Guard”—Todd Combs and Ted Weschler. Stakes in Alphabet (GOOGL), Amazon (AMZN), and Mastercard (MA) represent the tech-forward lean of the younger managers. These are “Growth at a Reasonable Price” (GARP) plays. Alphabet, now a top-10 holding at ~2.2%, reflects a belief that AI, despite the hype, is a utility that will eventually be dominated by those with the biggest data moats.

The Neighbor’s Verdict: Cash is a Strategy

The most important “holding” in the Berkshire portfolio isn’t a stock at all—it’s the Cash Pile. As of early 2026, Berkshire’s cash and equivalents are at record levels. This is the ultimate “Munger-style” move.

In a market that is “Policy-Captured” and potentially overvalued, the most dignified thing to do is wait. The cash isn’t “idle”; it is an Option. It is the ability to act when the “Neighbor” panics. Whether it’s another massive acquisition like OxyChem or a rescue of a failing financial giant, the cash pile ensures that Berkshire remains the “Lender of Last Resort” in the private sector.

Summary

Berkshire Hathaway in 2026 is a study in Resilience over Efficiency. It has sacrificed the high-octane growth of a 100% Apple portfolio for a diversified, cash-rich fortress. It is a portfolio designed not to win every single year, but to never be defeated in any year.

Greg Abel has inherited a “Latticework” of businesses that are less dependent on the mood of the Fed and more dependent on the fundamental needs of humanity: energy, insurance, credit, and a cold drink on a hot day. It is, quite simply, the most “Dignified” portfolio on the tape.